Works: finance them for free thanks to the purchase of real estate loans

Why renegotiate your mortgage? Our analysis

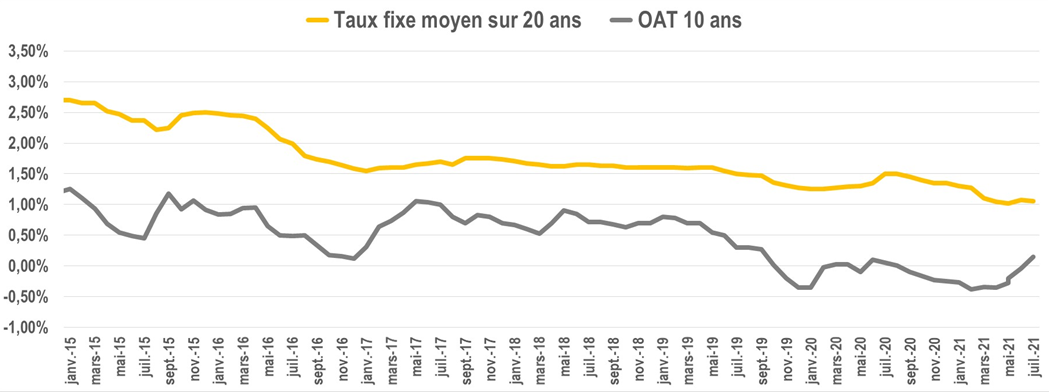

Sharp drop in mortgage rates

It was the average borrowing rate over 20 years, 6 years ago.

1% in 2021

This is what you can negotiate for a home loan over the same duration in 2021. Lower interest rates also means budgeting for the same repayment.

Financing conditions have been falling for more than 10 years, a drop amplified by the health crisis in 2020.

This is an opportunity to renovate your home, while keeping the same purchasing power.

Finance work with the same monthly payments

With the same monthly payment, but with more advantageous conditions, this is an opportunity to finance work without affecting your monthly budget. Each month, you will pay the same amount.

Want a pergola, a rainwater tank, a double-flow VMC? Integrate this work when renegotiating your mortgage and continue to repay the same monthly payment.

Example of a mortgage buyout, with a work envelope of 25,000 euros

Initial home loan

Capital remaining due: 336,891 euros

Monthly payment with insurance: 2,181 euros

Fixed rate at 1.70%

Remaining term: 218 months

New loan with 25,000 euros of work

New monthly payment: €2,180 with €25,000 of work

Fixed rate at 0.75%

New financing term: 218 months

What works can be included when renegotiating your mortgage?

Everything that remains "physically" in the accommodation: kitchen, inground swimming pool, pergola, tank, etc. An estimate and then an invoice are required by the bank to ensure the proper use of the funds.

In contrast, furniture, household appliances, everyday consumer goods do not fall within the scope of real estate financing.

These objects are financed by consumer credit, with different conditions and regulations.

Difference between a home loan buyout and a credit consolidation?

A repurchase of mortgage concerns only what affects your real estate (the property itself + its long-term facilities).

Car, consumption and revolving credits cannot be financed during this operation.

A credit consolidation includes any type of debt. But beware, these operations are financed by other types of banking institutions. The proposed conditions and fees are much higher in this second case.

What are the fees for the borrower?

Early repayment indemnity

Redeeming your credit is a breach of contract. In this case, the bank that lent you money will ask you either:

- 3% of the capital remaining due

- Or 6 months of interest at the time of redemption.

To know the most favorable amount, it's very simple: take your amortization table (in your mortgage contract).

Write down the amount of your outstanding principal (in other words, what you still owe the bank), as well as the amount of interest that month.

Example :

Capital remaining due : €176,872 or Interest due on 10/2021: €266.25

The compensation requested will therefore be the most favorable of:

€176,872 x 3% = €5,306

Or 266.25 × 6 = €1,597.25.

We therefore include €1,597 in reimbursement costst anticipated in the new financing.

Possible exemptions:

- Sale of housing following a change of place of work or that of the person with whom you live

- Dismissal

- Death of one of the borrowers

Application and brokerage fees

If you go through a broker and a bank, processing fees are required. Since financing conditions are currently very low, it is very difficult to be exempt from these costs.

These fees are calculated according to the amount of the loan or according to a fixed amount. Each establishment applies its own policy.

Bank guarantee

Any banking establishment will ask for the establishment of a guarantee during a mortgage: Housing loan, internal guarantee company, mortgage.

Note that if you have subscribed to Crédit Logement for the initial loan, part of the initial costs will be reimbursed.

Can you renegotiate your mortgage multiple times?

You can do this as many times as you want. It is up to you to check the economic relevance of the operation and its long-term viability.

Indeed, if you wish to resell the accommodation soon, do not launch the operation: the costs inherent in the repurchase are amortized over the medium term.

Conclusion

If you signed your loan offer several years ago, now is a good time to renegotiate your mortgage.

Indulge yourself by integrating the work of your dreams. So, take out your loan offer and make an appointment with your banker or a broker!

This will allow you to check the relevance of the operation, the financial feasibility and the potential gain.

We can put you in touch with our broker partner in order to obtain comparative offers and a complete simulation: write directly to contact@lacentrale-eco.com .